Remember, not every stock will pay a dividend. ferrantraite/Getty Images

A qualified dividend is a dividend that's taxed at a lower rate for meeting certain criteria.

Criteria includes shares from domestic corporations and certain qualifying foreign companies, which must be held for a specific period of time, known as the holding period.

These dividends are taxed federally at the capital gains rate, which varies based on an investor's MAGI and taxable income.

For investors, dividends can be one of the most rewarding features of owning a stock. Dividends are payments that shareholders receive from a company's earnings. This can be seen as a thank you note in the form of cash for investing in the company.

Receiving a dividend payment for the investor is a source of income, and like most forms of income, there can be tax implications. Dividends can be taxed either as ordinary dividends (also known as nonqualified) or as qualified dividends, with each of these classifications carrying significant differences in tax rates.

What is a qualified dividend?

Qualified dividends are dividend payments that are taxed at the long-term capital gains rate, which is lower than the ordinary income tax rates. For a dividend to be qualified there are certain criteria that must be met, according to the IRS.

For stocks the criteria is:

The stock must be held for at least 61 continuous days, unhedged, out of the 121-day period, beginning 60 days before the ex-dividend date.

In some cases, like with preferred stock, it must be held for 91 out of the 181-day period, beginning 90 continuous days before the ex-dividend date.

What is the ex-dividend date? This is the date on which the stock will trade without its dividend rights, meaning the previous owner will be entitled to the next dividend payment. Unhedged means that you cannot have any options like puts or calls that are related to the stock – and you cannot have any short sales during the period.

Understanding how qualified dividends work

From the investor's perspective, qualified dividends procedurally work in similar ways as ordinary dividends - with one exception. "It all comes down to how they're taxed," says Akeiva M. Ellis, MSFP, Certified Financial Planner financial education specialist at Ballentine Partners. "Regular dividends get taxed at your ordinary income tax rate, just like your wages and other earned income. Qualified dividends are currently taxed at the lower, preferential rates that long-term capital gains income gets," Ellis notes.

In addition to the holding period requirements, the IRS specifies that qualified dividends must be paid to an investor by a US company or a qualified foreign company. But not every dividend received will be qualified, even if you meet the holding period. "Some dividends do not count as qualified dividends. These include those paid by Real Estate Investment Trusts (REITs), employee stock options, and tax-exempt organizations," says Ellis. In addition to those, dividends paid on deposits at banks and credit unions do not count as qualified dividends and are instead reported as interest income, taxed at ordinary income rates.

Qualified dividend tax rates

Qualified dividends were not a part of the tax code until the Jobs and Growth Tax Relief Reconciliation Act of 2003. Prior to this, all dividends were taxed at the ordinary income tax rate. The argument for policymakers at the time was that the lower rates for qualified dividends would incentivize companies to reward long-term investors with higher dividend payments. If successful, that money would then be circulated through the economy and generate growth.

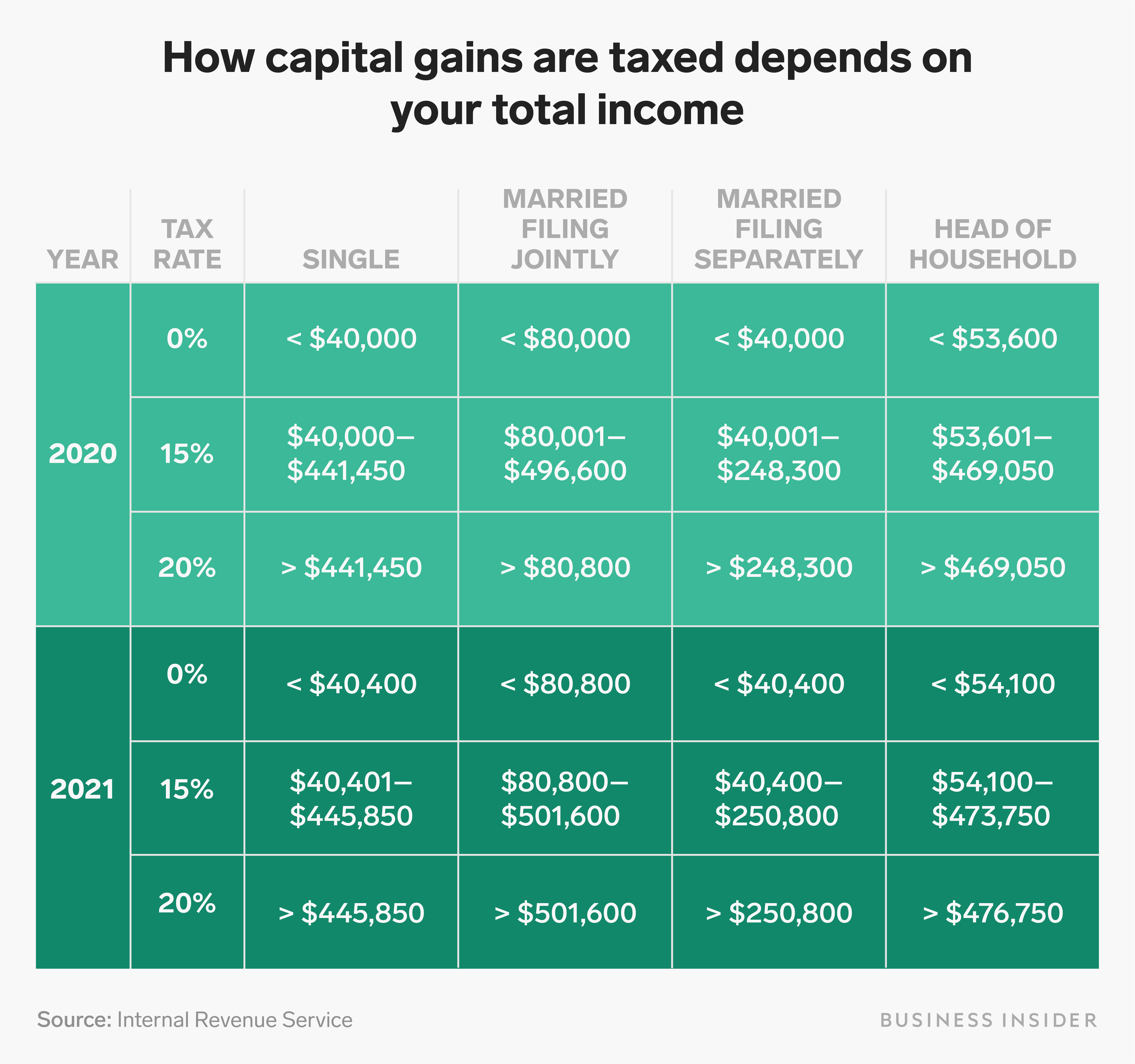

Here's a breakdown of the tax rates:

Capital gains tax rates have changed slightly from 2020 and 2021. Yuqing Liu/Business Insider

Remember, not every stock will pay a dividend. If you receive any dividend in your investing account you should receive Form 1099-DIV at the end of the year from your brokerage firm. The amount you have earned in qualified dividends should appear in box 1b.

Retirement accounts can nullify the impact of taxes on dividends. For pre-tax retirement accounts like a 401(k) and Traditional IRA, all taxes are deferred until withdrawal, at which point only ordinary income taxes will be applied, and the annual taxes on dividends will be avoided.

For after-tax retirement accounts like a Roth IRA or Roth 401(k), withdrawals can be tax free including any dividend income generated under certain conditions. In the case of a Roth IRA, those conditions are that you are 59.5 years old and you have had the account for at least five years.

Ordinary dividends vs. qualified dividends

As the name implies, ordinary dividends - sometimes referred to as nonqualified dividends - are taxed at the ordinary capital gains rates. The main difference between ordinary dividends and qualified dividends are how they're taxed:

Ordinary dividends

Qualified dividends

Taxed at ordinary income tax rates of: 10%, 12%, 22%, 24%, 32%, 35%, and 37%

Taxed at the capital gains tax rates of: 0%, 10% and 15%

Of course, another difference between the two is that qualified dividends must meet certain criteria, like the holding period, which we mentioned before.

The financial takeaway

Taxes can have a significant impact on your investing strategy and your overall returns. It is important to understand how to manage your investments in a way that minimizes your tax liability and maximizes your financial security, and qualified dividends can be one important piece to that strategy.